In today’s dynamic financial landscape, many of us feel overwhelmed by fluctuating incomes, rising expenses, and the constant pressure to plan for an uncertain future. Traditional budgets can be rigid, demanding constant tracking and leading to burnout. What if there was a more intuitive, adaptable way to manage money? Enter the Money Map: a personalized visual financial blueprint that transforms how you perceive and direct your cash flow, empowering you to make confident decisions about every dollar.

By adopting a Money Map, you eliminate guesswork, reduce stress, and build momentum toward meaningful goals. Imagine waking up each day knowing exactly where your income will go—bills are covered, savings are advancing, debts are shrinking, and investments are growing. This article will guide you through understanding, creating, and maintaining a Money Map that aligns with your dreams, adapting to life’s twists and turns along the way.

Understanding the Money Map Blueprint

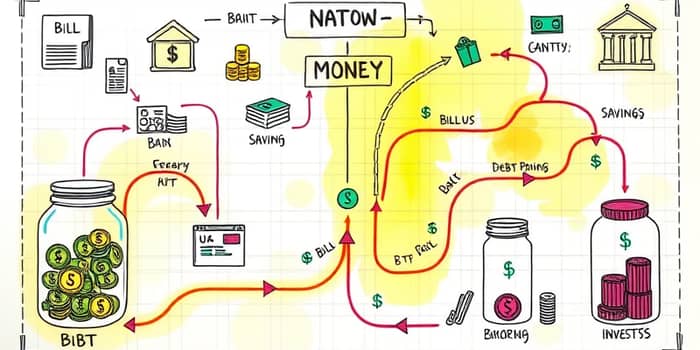

A Money Map is more than a budget; it is a living diagram depicting where every dollar goes in real time. Rather than tracking every purchase, you assign income to purpose-driven buckets—fixed expenses, variable spending, savings, debt repayment, and investments. The map is dynamic, evolving with your income changes, seasonal expenses, or surprise costs.

At its core, the Money Map fosters a full-picture view of cash flow, connecting each financial decision back to your overarching life goals. Whether you dream of early retirement, world travel, or launching a business, the Money Map ensures your daily habits fuel those bigger aspirations.

Key Components of Your Money Map

Crafting an effective Money Map involves identifying essential elements and visualizing their relationships. While the design is uniquely yours, every map typically includes:

- Income Sources: All after-tax earnings, from paychecks and freelance gigs to rental revenue.

- Fixed Expenses: Necessities like rent, utilities, insurance, and loan payments, usually color-coded in red for priority.

- Variable Spending: Discretionary areas such as groceries, dining out, entertainment, and shopping—zones for possible adjustment.

- Savings Goals: Emergency funds, vacation pools, and special-purpose accounts, often highlighted in blue to track progress visually.

- Debt Repayment: Targeted allocations to credit cards or loans, commonly marked in orange to emphasize reduction milestones.

- Investments: Automated contributions toward retirement accounts or brokerage portfolios, tailored to time horizons and risk tolerance.

These elements work in concert, highlighting how each dollar supports daily needs and long-term dreams. When you color-code and position buckets on your map, you gain a visceral sense of ownership over your financial journey.

Money Map vs Traditional Methods

Comparing a Money Map to other financial approaches reveals its unique strengths and why it resonates with modern earners:

Real-Life Example: Sarah’s Transformation

Sarah, a graphic designer juggling multiple gigs, struggled to keep bills paid while saving for a dream vacation. Upon adopting a Money Map, she created clear buckets for rent, utilities, supplies, emergency fund, and travel goals. By automating transfers, Sarah eliminated late fees and built a travel fund in under six months. Her map revealed that cutting back on dining out by 15 percent could fuel her vacation without sacrificing lifestyle—an insight she’d never discovered with a rigid budget.

By reviewing her map monthly, Sarah identified a recurring subscription she no longer used, redirecting those funds into her emergency savings. The visual clarity empowered her, turning financial stress into excitement about reaching new milestones and building true confidence in her money decisions.

Six Steps to Create and Maintain Your Map

Building a Money Map is straightforward when broken down into actionable steps. Treat it as a living guide that you revisit regularly:

- Gather Data: Compile your after-tax income and pull spending reports from credit cards or aggregator tools to understand current habits.

- Visualize Flow: Draw the chart, placing income at the center and branching outward to expenses, savings, debt, and investments. Use color coding to differentiate buckets.

- Automate: Set up direct deposits or transfers into designated accounts for bills, savings goals, and investment contributions.

- Align with Goals: Connect each bucket to short-term objectives like an upcoming vacation and long-term dreams such as retirement or a down payment on a home.

- Review & Adjust: Conduct monthly check-ins to account for income changes, unexpected bills, or shifting priorities. Update allocations as needed.

- Track Progress: Monitor goal achievements on your map, spot cash flow leaks like unused subscriptions, and challenge yourself with periodic no-buy or savings sprints.

Real-World Impact and Benefits

Adopting a Money Map can transform your financial outlook, yielding practical and emotional rewards. Key benefits include:

- Clarity & Confidence: Eliminate guesswork by knowing exactly how funds are allocated, reducing stress over money decisions.

- Progress Engine: Automation creates unstoppable momentum, ensuring steady advances toward each goal.

- Flexibility for Modern Life: Perfect for variable-income earners or gig workers, prioritizing intention over restrictive limits.

- Holistic Integration: Seamlessly links day-to-day habits with broader advisory plans, tax considerations, and market strategies.

- Tools for Success: Leverage apps like Fruitful for combined tech and human guidance, or My Money Map to simulate net worth and cash flow scenarios.

Partnering with Professionals and Emerging Tools

While a DIY Money Map empowers you to take control, collaborating with financial professionals can add depth and accountability. Advisors and planners offer personalized insights, stress-testing your map against market shifts or tax changes.

Looking ahead, financial technology is integrating AI-driven insights that detect shifting spending patterns, suggest optimized allocations, and even forecast potential market impacts on investments. Tools tailored for remote workers and digital nomads automate currency conversion and tax withholding, ensuring your Money Map remains accurate across borders.

Your Money Map is not just a plan but a journey. As you watch each bucket grow, defeat debt, and fuel investments, you’ll experience a sense of mastery and hope. Begin crafting your Money Map today—your future self will thank you for the clarity, confidence, and freedom it delivers.

References

- https://www.fruitful.com/post/what-is-a-money-map

- https://www.preparedretirementinstitute.com/blog/money-maps-flexible-approach-financial-freedom

- https://business.seminolebusiness.org/news/details/understanding-financial-planning-your-roadmap-to-financial-well-being

- https://financialfootwork.com/blogs/my-money-blog/money-mapping

- https://www.asset-map.com/blog/strategic-financial-planning

- https://www.youtube.com/watch?v=b-VJGqfwNzo

- https://www.provwealth.com/what-is-a-financial-plan-by-lee-f-hediger/

- https://mymoneymap.io

- https://www.nerdwallet.com/financial-advisors/learn/what-is-a-financial-plan